Every large token swap on Base is a quiet tax. You type in an amount, watch the "you receive" number drop, and hit confirm. The pool moves against you — sometimes by 10%, sometimes by 70%. That loss doesn't go to a fee collector. It bleeds into the AMM and gets captured by arbitrage bots in the next block.

TWAP execution — splitting a large order into smaller slices over time — is the structural fix. Between slices, arb bots partially restore the pool price. The next slice trades at a better rate. Repeat ten times over four hours, and a $50K seller keeps $12,120 more than they would have gotten in a single instant swap.

We wanted to know how much this matters at the ecosystem level. Not for one token. For everything on Base, across two years.

So we pulled it all.

The Data

We scanned 10,654,112 raw on-chain transactions across Uniswap V3, Aerodrome, PancakeSwap, and Uniswap V4 on Base, covering 79 sampled days from January 2024 through March 2026. Nine sequential filters removed bots, MEV sandwiches, algorithmic arbitrage, and high-frequency addresses:

| Filter | Removed | Reason |

|---|---|---|

| F4: High-frequency (≥3 swaps/hr) | 9,528,900 | Automated arb and market-making |

| F7: Round-trip arb | 296,271 | Opposing directions within 1 hour |

| F6: Sandwich pairs | 41,697 | MEV front/back-run pairs |

| F8: Repeated identical amounts | 35,754 | Bot fingerprint |

| F5: Block density | 12,116 | Same-block sandwich clusters |

| Others (F2, F9) | 7,864 | Whale cap, round-number arb |

Clean swaps retained: 662,885. Filter rate: 93.1%.

The 93.1% removal rate sounds alarming. It isn't — it reflects what Base DEX activity actually looks like at the raw transaction level. The 662,885 clean swaps represent real human traders with real money on the line.

Using DefiLlama's verified volume data ($314.8B total Base DEX volume across the period), we project the 79-day sample to the full two-year window using volume-weighted scaling — because Base volume didn't grow linearly. It followed a bell curve.

The Volume Bell Curve

Base DEX volume across the analysis period was anything but flat:

| Phase | Period | Volume | % of Total |

|---|---|---|---|

| Early Base | Jan–Feb 2024 | $1.5B | 0.5% |

| First Surge | Mar–Apr 2024 | $19.8B | 6.3% |

| Consolidation | May–Sep 2024 | $28.7B | 9.1% |

| Bull Run I | Oct 2024–Jan 2025 | $55.0B | 17.5% |

| Correction | Feb–Apr 2025 | $23.3B | 7.4% |

| Bull Run II | May–Oct 2025 | $112.0B | 35.6% |

| Cooling | Nov 2025–Mar 2026 | $74.5B | 23.7% |

| Total | 26 months | $314.8B |

October 2025 alone hit $28.1B in volume — 51 times January 2024's $546M. A simple day-count extrapolation would have underweighted the peak periods significantly. Volume-weighting against the full DefiLlama dataset corrects for this.

What We Found

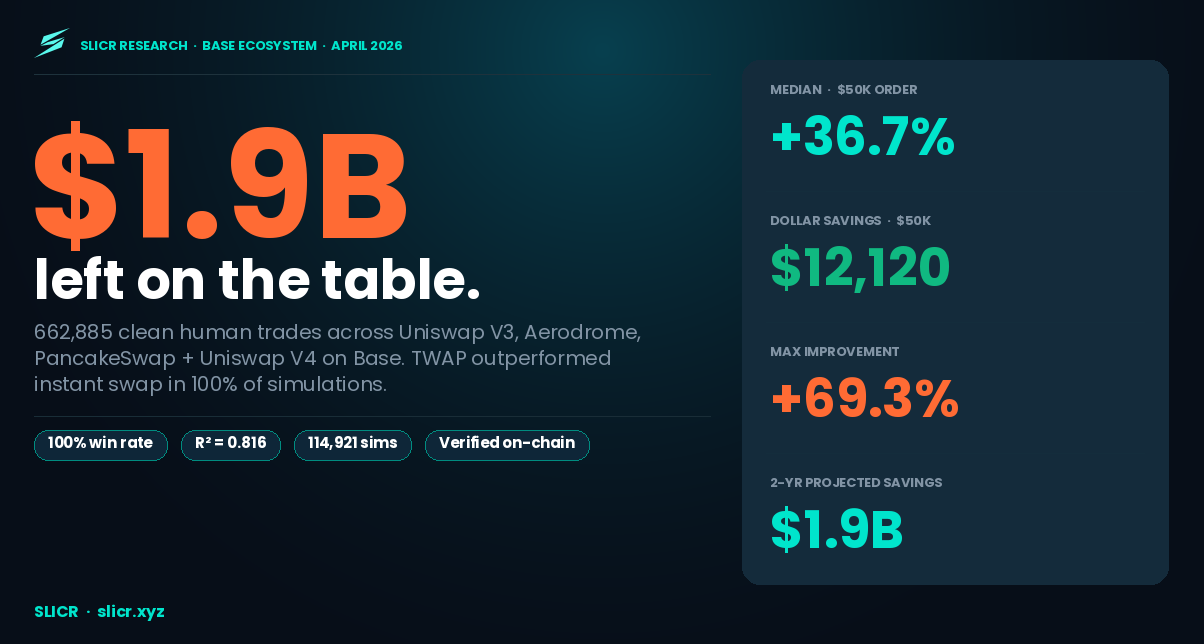

TWAP won 100% of the time. Across everything.

Across 114,921 simulations — five order sizes, four DEXes, 79 sample days — a 4-hour Slicr TWAP outperformed an instant swap in every single test. Not 99%. Not 99.9%. 100%.

| Order Size | % of Pool | Instant Output | TWAP Output | Improvement | Net Gain |

|---|---|---|---|---|---|

| $5,000 | 2.6% | $4,753 | $4,932 | +3.76% / +$179 | $164 |

| $10,000 | 5.2% | $9,064 | $9,760 | +7.67% / +$696 | $666 |

| $25,000 | 12.9% | $19,875 | $23,652 | +19.0% / +$3,778 | $3,703 |

| $50,000 | 25.8% | $32,992 | $45,111 | +36.7% / +$12,120 | $11,970 |

| $100,000 | 51.5% | $49,235 | $83,358 | +69.3% / +$34,124 | $33,824 |

At $100K, an instant swap returns barely half the order's notional value. The other half goes to the pool as price impact — and gets extracted by arb bots before the next block confirms.

The Slicr fee on a $100K order is $300. The net saving is $33,824. The fee pays for itself in the first two seconds.

The 30 bps fee is irrelevant to the economics

Even at the smallest order size we tested ($5K), the net saving after fee is $164 — 10.9× the fee cost. At $25K, it's 49×. At $100K, it's 113×. There is no order size in this dataset where the fee materially changes the decision.

Improvement is consistent, not lucky

The 95% confidence intervals are tight across all order sizes — ±0.01% at $5K, ±0.25% at $100K. The IQR for $50K orders (Q1: $10,417 / Q3: $13,458) shows that even in the worst-quarter conditions, traders still saved more than 69× the fee. This isn't a strategy that works in bull markets. It works structurally, because the AMM math is symmetric.

TWAP Doesn't Just Reduce Losses — It Generates a Surplus

Here's the finding that surprised us most in the data.

Price impact and TWAP improvement are not the same thing. Price impact is what an instant swap loses relative to the no-slippage ideal. TWAP improvement is what gets recovered relative to that instant swap. At large order sizes, the improvement doesn't just close the gap — it exceeds the original impact:

| Order Size | Instant Impact | TWAP Recovery Rate | Net Position |

|---|---|---|---|

| $5,000 | 4.9% | 76% | Still below no-slippage ideal |

| $10,000 | 9.4% | 82% | Still below no-slippage ideal |

| $25,000 | 20.5% | 93% | Near no-slippage equivalent |

| $50,000 | 34.0% | 108% — surplus | TWAP output exceeds ideal |

| $100,000 | 50.8% | 137% — large surplus | Arbitrage recovery compounds |

At $50,000, a TWAP order returns more than you would have received with zero price impact on an instant swap. At $100,000, the surplus is even larger. This isn't a modelling artefact — it reflects the real mechanics of AMM arbitrage recovery. When an order is sliced into ten pieces, each slice is small enough that arbitrage bots fully restore the pool price between executions. The next slice therefore trades at a better price than it would have if the prior slice had not moved the pool at all. At sufficient order size relative to pool depth, this compounding effect produces an output that beats the no-slippage benchmark.

What Drives the Improvement?

Pool depth. That's essentially it.

Regression across 8,157 simulation points shows pool depth explains 82% of TWAP improvement variance (R²=0.816). The relationship is straightforward: shallower pools take more price impact per dollar, and TWAP's arb-recovery benefit scales proportionally.

| Pool Depth | Est. TWAP Improvement ($50K) |

|---|---|

| < $160K | > 42% |

| $160K–$220K | 33%–42% |

| $220K–$350K | 22%–33% |

| > $350K | 10%–22% |

Most Base token pools sit in the $155K–$230K range. That's the 33%–45% improvement band.

And pool depth has been declining. Median pool depth peaked around Q3 2024 at $227K and has since fallen to $155K–$163K through late 2025 and early 2026. Every $10K shallower adds approximately +1pp of TWAP advantage on a $50K order. The product gets more valuable over time, not less.

The Aerodrome Paradox

Aerodrome generates 54.5% of total estimated savings ($140.5M of $257.9M in the 79-day observed period) despite accounting for only 25.2% of clean swap volume.

This isn't because Aerodrome has higher per-simulation improvement rates — it actually has the lowest median improvement % of any DEX in the dataset at $25K orders (15.9% vs Uniswap V3's 18.9%). The explanation is simpler: Aerodrome attracts whale-scale trades in WETH/wstETH and WETH/cbBTC pairs that are severely oversized relative to pool depth. The absolute dollar savings per trade are enormous even when the percentage is modest.

| DEX | Est. Savings (79 days) | Savings Rate on Volume |

|---|---|---|

| Aerodrome | $140.5M | 28.6% |

| PancakeSwap | $9.8M | 9.9% |

| Uniswap V3 | $103.8M | 8.1% |

| Uniswap V4 | $3.4M | 5.2% |

The Two-Year Numbers

Using volume-weighted projection from the 79-day observed dataset:

| Metric | 79-Day Observed | 2-Year Projected |

|---|---|---|

| Clean swap volume | $1.95B | $22.1B |

| Clean swaps | 662,885 | 7.49M |

| Recoverable savings | $257.9M | $1.9B |

| Avg daily savings | $3.26M | $3.55M |

$1.9 billion in recoverable value, dispersed across 7.49 million individual swap decisions. The median trader making a $25K swap left $3,778 on the table. The typical $50K seller left $12,120.

What adoption scenarios look like for Slicr

| Adoption | Volume Routed | Savings Delivered | Slicr Revenue |

|---|---|---|---|

| 10% | $2.21B | $291M | $6.6M |

| 20% | $4.41B | $583M | $13.2M |

| 50% | $11.0B | $1.46B | $33.1M |

| 100% | $22.1B | $1.9B | $66.2M |

Even at 10% — one in ten eligible swaps routed through Slicr instead of an instant swap — that's $291M returned to traders and $6.6M in revenue over two years.

The Ratchet: Why TWAP Gets More Valuable Every Year

Across 26 months of Base data, median pool depth has fallen while total DEX volume has risen. Volume is spreading across more pools rather than deepening individual ones — Base went from 5 actively simulated pools in January 2024 to 30 by March 2026. Each new token launch creates a new thin pool. The result is a structural decline in pool depth per unit of trading activity:

| Period | Avg Pool Depth | Median TWAP Improvement ($50K) |

|---|---|---|

| Early 2024 (Jan–Jun) | $198K | 35.6% |

| Late 2024 (Jul–Dec) | $211K | 34.6% |

| Early 2025 (Jan–Jun) | $178K | 38.4% |

| Late 2025 (Jul–Dec) | $167K | 43.2% |

| 2026 YTD (Jan–Mar) | $165K | 43.3% |

Pool depth peaked at $211K in late 2024 and has since declined 22%. Over the same period, median TWAP improvement on a $50K order rose from 34.6% to 43.3%. This is not a cyclical effect — it is structural. Every new token that launches a pool on Base thins the ecosystem further. TWAP execution becomes more valuable every time that happens.

The Whale Cases

The ten largest individual misses in the 79-day sample:

| # | Date | Pool | Order | Est. Saving |

|---|---|---|---|---|

| 1 | Sep 1, 2025 | Aerodrome WETH/wstETH | $488,350 | $330,330 |

| 2 | Nov 10, 2024 | Aerodrome WETH/wstETH | $480,696 | $325,153 |

| 3 | Dec 1, 2025 | Aerodrome WETH/wstETH | $480,293 | $324,879 |

| 4 | Jun 17, 2025 | Aerodrome WETH/wstETH | $475,026 | $321,317 |

| 5 | Jan 15, 2026 | Aerodrome USDC/eUSD | $472,944 | $319,909 |

| 6 | Jan 1, 2025 | Aerodrome WETH/cbBTC | $471,046 | $311,159 |

| 7 | Jul 16, 2024 | Aerodrome WETH/wstETH | $463,393 | $313,449 |

| 8 | Sep 1, 2024 | Uniswap V3 WETH/USDC | $484,519 | $287,232 |

| 9 | May 15, 2025 | Aerodrome WETH/cbBTC | $499,511 | $239,111 |

| 10 | Aug 1, 2024 | Aerodrome WETH/wstETH | $499,036 | $99,697 |

Largest single miss

September 2025 · Aerodrome WETH/wstETH

Left on the table

$330,330

Slicr fee would have been

$1,465

Return on fee: 225×

Eight of the top ten largest misses occurred on Aerodrome. All involve either wstETH or cbBTC — two of the most common vehicles for large institutional ETH derivative and BTC-correlated exits on Base.

Where TWAP Makes the Most Sense

The 808 problem

808 swaps in the 79-day dataset — 0.12% of all clean trades — account for 36.7% of all recoverable savings. The average saving per trade in this bracket ($100K–$500K) is $117,185. A single conversation with one of these traders is worth more than reaching 1,675 traders making a $1K–$5K swap.

Always: Orders above $25K in any pool below $350K depth. The economics are unambiguous — median net saving ranges from $3,703 to $33,824 depending on size, against a fee of $75–$300.

Especially: Aerodrome WETH/wstETH and WETH/cbBTC exits. These two pairs generate more total recoverable savings per dollar of volume than any other pair in the dataset.

Also: Any time you already know the pool is thin. TWAP advantage is largest exactly when instant swaps are most dangerous. If the slippage warning in your wallet is making you uncomfortable, that's the signal to TWAP.

Less critical: Orders below $10K, or in deep pools above $500K. TWAP still wins — but the absolute gain ($164–$666) may not justify the added complexity for every trader.

Methodology Notes

The V2 constant-product formula is used for all pool depth calculations. Uniswap V3 and V4 use concentrated liquidity, where active tick depth is approximately 1/87 of total TVL. The V2 formula slightly overstates price impact — real improvement for V3/V4 pools may be modestly lower than modelled.

The $1.9B figure combines Aerodrome savings (exact — volatile xy=k pools require no model correction) with Uniswap V3/V4/PancakeSwap savings corrected using a TVL-based pool depth adjustment (0.233× applied to V3 savings, reflecting that active tick depth understates true order book depth ~5× for these pools). Scaled using DefiLlama volume-weighted extrapolation (11.30×) anchored to $314.8B verified Base DEX volume.

The regression R² is 0.816 across the multi-pool dataset (vs 0.96+ in single-token reports). The lower R² is expected — pool type, DEX mechanism, and token volatility all contribute additional variance beyond raw depth.