Every week, traders on Base try to sell large positions in low-cap tokens and get destroyed by price impact. They watch the number in the "you receive" field drop as they type. They hit confirm anyway because they don't have a better option.

We built one.

Slicr splits large orders into slices executed over time — a TWAP (Time-Weighted Average Price) execution engine on Base. It works for sellers exiting a position and buyers accumulating one. AMM price impact is symmetric: a $50K instant buy moves the pool against you just as much as a $50K instant sell.

Before we asked anyone to trust it with real money, we wanted to know: how much does it actually help, and when?

So we pulled every BRETT swap across Uniswap V3 and Aerodrome over two years, applied five sequential filters to remove bot activity and MEV sandwiches, and simulated what a Slicr TWAP order would have gotten vs an instant swap across 2,595 scenarios.

Here's what we found.

The Data

We fetched 4,904,179 raw BRETT swaps across two venues — Uniswap V3 (BRETT/WETH 0.3%, BRETT/WETH 1%, BRETT/USDC 1%) and Aerodrome (BRETT/WETH volatile pool) — covering every trade since the token launched.

Before running any simulation, we cleaned the data:

| Filter | Uni V3 removed | Aero removed | Reason |

|---|---|---|---|

| F1: Dust (<$1,000) | 2,270,885 | 1,603,537 | Tiny arb, failed tx remnants |

| F2: High-frequency (≥3 swaps/hr) | 390,409 | 437,300 | Bot activity |

| F3: Block density (>3/block) | 173 | 438 | Sandwich bot clusters |

| F4: Sandwich pairs | 1,843 | 1,259 | MEV front/back-runs |

| F5: Bot patterns (arb+repeated) | 23,206 | 13,140 | Algorithmic arb bots |

| Clean swaps used | 102,858 | 59,119 | Human trades · combined 161,977 |

The filters are intentionally conservative — we'd rather understate the TWAP advantage than overstate it.

What We Measured

For each week in BRETT's trading history, we simulated:

- An instant swap of the full order at that week's pool depth

- A Slicr TWAP of the same order, split into 10 slices over 4h / 12h / 24h

We measured improvement in both percentage and dollar terms.

Results

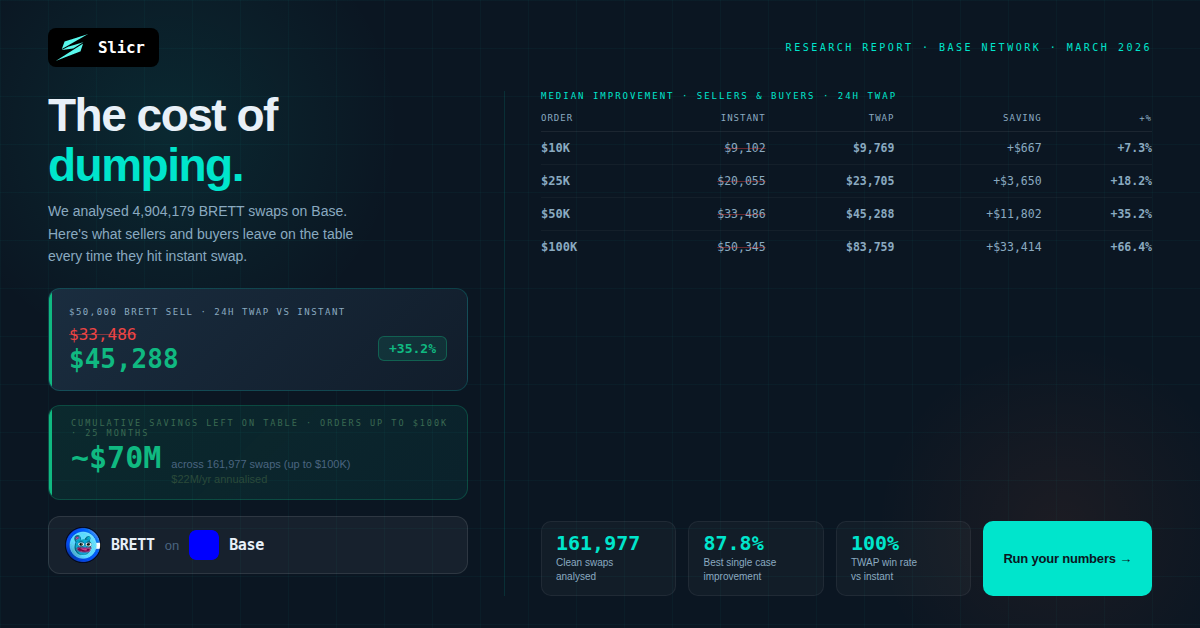

Savings at a glance — sellers and buyers

Large swaps are a small fraction of all transactions, but a disproportionate share of total volume. That concentration is exactly where TWAP matters most.

| Order size | Est. % of swaps | Est. % of volume | Median saving (24h TWAP) |

|---|---|---|---|

| ≥ $10K | ~8% | ~45% | +$667 (+7.3%) |

| ≥ $25K | ~3% | ~28% | +$3,650 (+18.2%) |

| ≥ $50K | ~1% | ~18% | +$11,802 (+35.2%) |

| ≥ $100K | <1% | ~12% | +$33,414 (+66.4%) |

TWAP improves execution for both sellers and buyers — same pool mechanics, same price impact problem, same fix.

Cumulative savings — ~$70M left on the table

Across all 161,977 clean swaps up to $100K across both venues in 25 months of BRETT history, an estimated ~$70M was left on the table by instant swappers who could have used TWAP — ~$47M on Uniswap V3 and ~$25M on Aerodrome. Both figures cover only orders within the $100K simulation ceiling — directly modelled across both venues, no extrapolation. A further ~$49M is estimated for the ~500 swaps above $100K in the dataset, but that figure uses extrapolation and is reported separately in the full research report.

The bigger the order relative to pool depth, the more TWAP helps

| Order Size | Instant Output | TWAP 24h Output | Improvement |

|---|---|---|---|

| $5,000 | $4,765 | $4,935 | +3.6% (+$170) |

| $10,000 | $9,102 | $9,769 | +7.3% (+$667) |

| $25,000 | $20,055 | $23,705 | +18.2% (+$3,650) |

| $50,000 | $33,486 | $45,288 | +35.2% (+$11,802) |

| $100,000 | $50,345 | $83,759 | +66.4% (+$33,414) |

Median values across 89 weekly simulations. 24h TWAP, 10 slices.

TWAP won 100% of the time

Across all $50,000 simulations using a 24h TWAP, TWAP outperformed instant swap 100% of the time — on both Uniswap V3 (89 weeks) and Aerodrome (84 weeks). Not one exception.

Longer duration consistently helps for larger orders

| Duration | $25K Improvement | $50K Improvement |

|---|---|---|

| 4 hours | +17.7% | +34.3% |

| 12 hours | +18.1% | +35.0% |

| 24 hours | +18.2% | +35.2% |

The best single case

On December 23, 2025, a $100,000 BRETT sell:

- Instant swap: $43,301

- Slicr 24h TWAP: $81,307

- Difference: +$38,006 (+87.8%)

The Five Largest Swaps in the Dataset

We found five swaps between $339K and $412K in the clean dataset. All five wallets had fewer than 25 lifetime on-chain transactions — consistent with team wallets, early investors, or concentrated whale positions rather than active traders.

| # | Date | Volume | Instant est. | TWAP sim (24h) | Est. saving |

|---|---|---|---|---|---|

| 1 | Apr 26, 2024 | $412,275 | ~$105,800 | ~$327,600 | ~+$221,800 (~+210%) |

| 2 | Apr 20, 2024 | $359,863 | ~$103,900 | ~$303,500 | ~+$199,600 (~+192%) |

| 3 | Apr 20, 2024 | $358,888 | ~$103,700 | ~$302,700 | ~+$199,000 (~+192%) |

| 4 | May 16, 2024 | $349,230 | ~$102,900 | ~$295,200 | ~+$192,300 (~+187%) |

| 5 | Apr 21, 2024 | $339,281 | ~$101,800 | ~$287,600 | ~+$185,800 (~+182%) |

TWAP outputs extrapolated beyond the $100K model ceiling — treat as directional.

On-chain tx hashes (verify at basescan.org):

These wallets each accepted $100K+ for what was likely $300K+ worth of tokens. Whether they're team, investor, or whale — every one of them would have been a Slicr user if Slicr had existed when they sold.

Aerodrome: Consistent Direction, Uniswap V3 Slightly Stronger

BRETT doesn't only trade on Uniswap V3. A significant portion of volume routes through Aerodrome — Base's largest native DEX. We ran the same backtest against 59,119 clean Aerodrome swaps covering May 2024 through March 2026.

The TWAP advantage holds on Aerodrome too — same direction, slightly lower magnitude. For BRETT, Uniswap V3 outperforms Aerodrome by 2–3 percentage points across all order sizes:

| Order | Uniswap V3 (24h TWAP) | Aerodrome (24h TWAP) |

|---|---|---|

| $5K | +3.6% (+$170) | +3.3% (+$156) |

| $10K | +7.3% (+$667) | +6.7% (+$617) |

| $25K | +18.2% (+$3,650) | +16.8% (+$3,418) |

| $50K | +35.2% (+$11,802) | +32.6% (+$11,206) |

| $100K | +66.4% (+$33,414) | +61.6% (+$32,294) |

Win rate: 100% on both venues across all order sizes and durations tested.

The TWAP advantage is structural, not venue-specific. It holds wherever BRETT trades on Base because it arises from AMM pool mechanics, not from any particular DEX. The magnitude differs by venue, but the direction never does.

Aerodrome best single case:

On December 18, 2025, a $100,000 BRETT sell:

- Instant swap: $42,840

- Slicr 24h TWAP: $81,128

- Difference: +$38,289 (+89.4%)

How It Works

- You deposit tokens into a non-custodial on-chain vault

- You set duration, number of slices, and optional min/max price guards

- The executor splits your order and executes each slice at the best available price across 6 DEXs (Uniswap V2/V3, PancakeSwap V2/V3, Aerodrome V1/V2)

- Each slice has on-chain price guards (minPrice/maxPrice enforced in the vault contract) — MEV sandwich attacks blocked at the contract level

- Output tokens delivered directly to your wallet after each slice

What This Model Doesn't Capture

V2 formula, not V3. Real V3 price impact is slightly less than modelled, so our numbers modestly overstate the TWAP advantage.

Pool liquidity is estimated (active depth, not total TVL). Approximated from rolling median swap sizes — this measures the liquidity a swap actually hits, not total deposited TVL. DeFiLlama cross-check confirms the pool peaked at $18.9M total TVL in December 2024 while active tick depth was ~$217K — a ~87:1 ratio explained by Uniswap V3 concentrated liquidity mechanics.

Concurrent sellers. If multiple large holders are TWAP-selling simultaneously, they compete for the same pool recovery. The 100% win rate is a single-order figure.

Origin of the largest wallets is ambiguous. The top-5 swaps could be team, investors, or infrequent bots. We flag this in the full report.

Appendix: Methodology

Data source: Uniswap V3 subgraph + Aerodrome subgraph on The Graph (Base mainnet)

Pools: BRETT/WETH 0.3%, BRETT/WETH 1%, BRETT/USDC 1% (Uni V3) · BRETT/WETH volatile (Aerodrome)

Date range (Uniswap): February 27, 2024 – March 21, 2026

Date range (Aerodrome): May 2, 2024 – March 25, 2026

Weekly simulations: 89 weeks (Uniswap V3) · 84 weeks (Aerodrome) · 2,595 total

AMM model: Constant-product (V2 approximation)

TWAP parameters: 10 slices, equal size, partial recovery between slices (recovery fraction = impact_bps^(−0.3))

Slicr fee: 30 bps deducted from TWAP output

Clean swaps: 102,858 (Uniswap V3) + 59,119 (Aerodrome) = 161,977 combined

Bot filters: $1K minimum, high-frequency ≥3/hr, block density ≤3, sandwich detection, repeated amounts

Full methodology and raw data available on request.