Vitalik Flagged a 2% Slippage Tax. We Tested It Two Ways.

Published June 2026 · 6 min read · slicr.xyz

On June 1, Vitalik Buterin posted a proposal for building index-tracking assets on top of options instead of debt. The mechanism is elegant: split one ETH into a (P, N) pair so the P-asset holder gets stable, USD-like exposure with no liquidation risk, ever. No collateral ratios, no liquidation cascades, no debt at all.

But the post flags one problem honestly, and it's a big one. To stay stable, the holder can't hold to maturity — that would re-introduce ETH exposure. So they have to roll strikes as the price moves. Every roll is a trade. Every trade pays slippage. In Vitalik's own words:

“It is very easy to lose 2% per year or more from multiple rounds of slippage, and this is the largest risk by which this whole scheme might become uncompetitive.”

That sentence is the whole ballgame. A scheme that's mechanically clean but bleeds 2%+ a year to execution costs loses to a plain index fund. So the question is simple: can the slippage tax actually be kept under that bar? The post also points at a possible fix:

“Rebalancing would be more like one-sided market making than like making an instant sell ... users' time preference will almost always be very low.”

So we tested both: the execution Slicr does today, and the passive one-sided making the post describes. They are not the same thing, and the difference is the most important part of this report — so let's be precise about it up front.

Two mechanisms, and which one is the product

This matters, so no hedging:

Slicr today is active TWAP slicing. It splits a large order into time-weighted slices and crosses the spread on each one, letting pool depth recover between slices, with on-chain price guards blocking MEV. It does not post passive liquidity. In this study, that active slicing is the line labeled “competent execution.” It is not a strawman — it is what the product actually does.

Passive one-sided making — posting resting liquidity and waiting for organic flow to fill it over days — is a different mechanism, and one Slicr has not shipped. In this study that is the line labeled “Slicr one-sided.” When you see the big calm-market number, read it as the prize that would justify building a maker mode, not as something Slicr delivers today.

How we tested it

No synthetic prices. We walked Vitalik's described roll algorithm across the real ETH/USD path on Base from January 2024 to March 2026 — 19,582 hourly price points, despiked for bad oracle prints, realized volatility 67%/yr. Walking that real path with his heuristic (strike S = X/2.5, roll when price falls to 1.5×S, 45-day maturity) produced 18 rolls over 2.23 years, about 8 a year.

Then we priced every one of those 18 rolls against real Uniswap V3 WETH/USDC tick liquidity— 78 dated snapshots of actual on-chain depth. We compared three styles on every roll: a naive single-venue dump (reference only), active TWAP slicing (Slicr today), and passive one-sided making (the roadmap mode). And to be clear about what we measured: these are the execution costs of the rolls themselves. They do not include the residual quadratic tracking drift that accrues between rolls — that is a separate cost the holder pays no matter how they execute.

Finding 1: Slicr's engine today already clears the bar

Here is the active-slicing line — the product as it exists — against Vitalik's 2%/yr threshold:

| Position | Slicr TWAP (today) | Crosses 2%/yr bar? |

|---|---|---|

| $100k | 0.45%/yr | No |

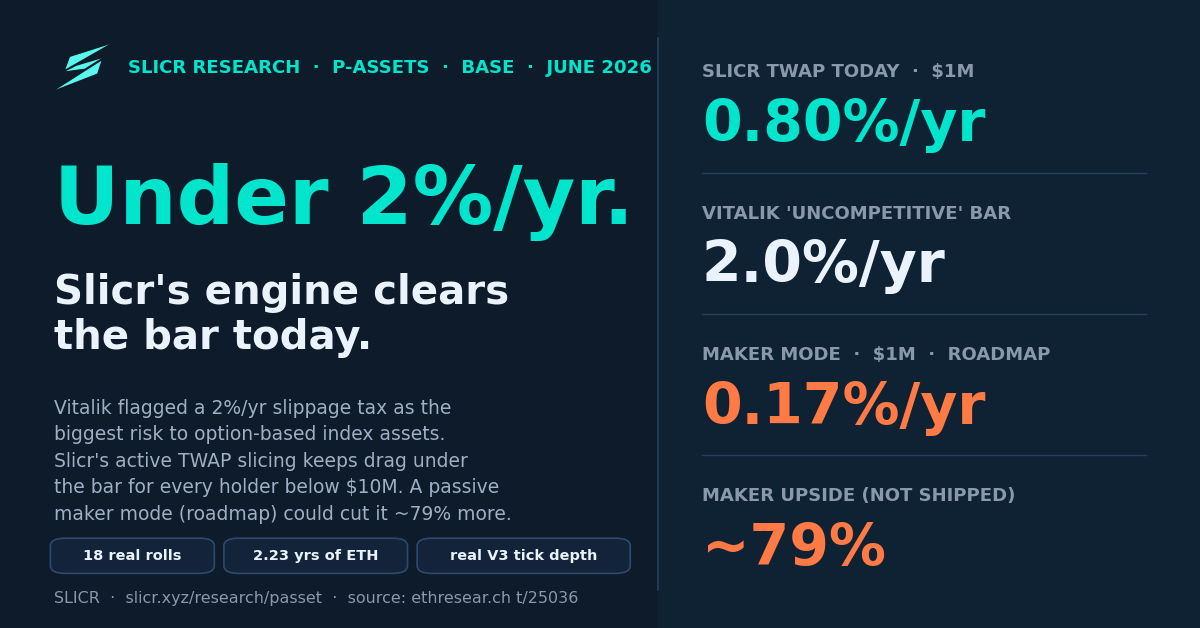

| $1M | 0.80%/yr | No |

| $5M | 1.97%/yr | No (just under) |

| $10M | 2.90%/yr | Yes |

Active TWAP slicing keeps rebalancing drag under the 2%/yr bar for every holder below $10M.That is the honest headline: the slippage tax Vitalik flags is real, but for ordinary holders it does not, on its own, sink the scheme — the execution tooling to stay under the bar already ships today.

Finding 2: A passive maker mode could cut drag a further ~79%

Now the opportunity. If Slicr posted passive one-sided liquidity instead of crossing the spread, a patient maker would earn the spread rather than pay it. In calm markets:

| Position | Slicr TWAP (today) | Passive maker (calm) | Maker upside |

|---|---|---|---|

| $50k | 0.29% | 0.10% | −64% |

| $100k | 0.45% | 0.10% | −78% |

| $1M | 0.80% | 0.17% | −79% |

| $5M | 1.97% | 0.36% | −82% |

We don't even count the market-making fees a maker would earn — leaving them out keeps the number conservative.

That ~79% reduction at $1M is real in the data — but it is the prize from a mode we would have to build, not a number we deliver now. And it comes with a serious catch.

The catch: everybody rolls at once

A passive maker assumes there is organic counterflow that wants the other side of your trade. Usually there is. But here is the structural problem unique to P-assets: every holder runs the same roll algorithm. When ETH falls through 1.5× the strike, the whole cohort wants to sell at the same time. The counterflow dries up at exactly the moment everyone needs it.

We modeled this as a crowded exit — flow capture drops to 1%, patience compresses to a single day, adverse selection rises. Under that stress, the maker-mode $1M drag rises from 0.17%/yr to 0.71%/yr — still under active slicing's 0.80%, but the edge has shrunk from ~79% to ~12%. At $10M the crowded number (2.85%) is essentially identical to active slicing (2.90%).

One honest footnote that cuts against us: in our model the crowded maker number stays belowslicing partly because any unfilled passive order falls back to active slicing — that fallback floors the cost. In a real cascade, a passive maker can do worse than slicing, because you are adversely filled as price drops straight through your resting order. So the crowded column is a floored, optimistic bound. If anything, that is the argument for slicing being the safer default exactly when the cohort panics.

One nuance in the maker's favor: maturity rolls are staggered across holders and don'tcrowd. Only price-trigger rolls do. Our crowded scenario applies the stress to every roll, so it is an upper bound on the crowding penalty. The real world sits between calm and fully crowded.

How robust is the ~79% number?

The maker-mode result rests on two assumptions: how much organic turnover exists, and how much one-sided flow a maker can capture. So we swept both. Here is maker-mode $1M drag (%/yr) across the grid, with active slicing at 0.80% as the reference:

| Capture \ Patience | 1 day | 3 day | 7 day |

|---|---|---|---|

| 1% | 0.65 | 0.46 | 0.38 |

| 2.5% | 0.45 | 0.24 | 0.24 |

| 5% | 0.18 | 0.17 | 0.17 |

| 10% | 0.12 | 0.12 | 0.12 |

Every cell beats slicing — though, again, the fallback floor flatters that. The maker upside is robust in direction, not in magnitude. A passive mode helps in calm markets. How much depends on conditions we cannot fully control.

What this doesn't capture

- Single path, single regime. One ETH/USD history, n=18 rolls, one volatility regime. The direction of every finding is robust; the magnitude is path- and regime-dependent. Higher vol should widen the gap by raising roll counts — but we show that as reasoning, not as a measured result across many paths.

- The active-slicing baseline is, if anything, a touch pessimistic. We used real Uniswap V3 depth on Base. Mainnet and aggregated routing are deeper, which would make slicing look even better and narrow the maker upside.

- We exclude earned market-making fees entirely. Counting them would improve every maker number. Leaving them out keeps the headline defensible.

- Gas is a flat per-roll cost. It dominates drag below ~$50k and is negligible above — which is why the small-size curve flattens.

- We measured execution cost, not tracking drift. Every figure prices the execution of the 18 rolls, not the quadratic drift between them. No execution style removes that drift.

The bottom line

The slippage tax Vitalik flags is real. But the tooling to keep it under the 2%/yr bar — active TWAP slicing — already ships, and it clears the bar for every holder below $10M. That is the part we can stand behind today.

The bigger calm-market saving comes from a passive maker mode we haven't built yet. The data makes a strong case for building it: in calm markets the upside is large. But in the synchronized stress that matters most for a P-asset cohort, that upside compresses, and a passive maker can fare worse than slicing. That trade-off is exactly the kind of thing worth resolving in code before claiming it in production — which is why we are publishing the analysis rather than a feature announcement.

That is the honest read. Slicr's slicing engine helps P-asset holders today. A maker mode might help them more, in the right conditions. We are not going to pretend the second thing is the first.

Full Research Report

The full study embeds the real ETH/USD path with every roll marked, per-roll cost breakdowns for a $1M holder, fill-rate curves by size, the complete sensitivity grid, and the full methodology.

View the full researchRun your own numbers

Price any order against real on-chain depth at slicr.xyz/backtest to see your projected saving in real time.

Try the backtest